On the evening of June 21, 2025, the Agency for the Regulation and Control of Strategic Mineral Markets in the DRC (ARECOMS), in light of the persistently high inventory levels in the market, decided to extend the temporary ban imposed on February 22 for an additional three months from the effective date of this decision. Below is the original document and its translation:

Temporary Decision on Extending the Suspension of Cobalt Exports from the Democratic Republic of the Congo

In accordance with Decision No. 001/ARECOMS/2025 of February 22, 2025, regarding the temporary suspension of cobalt exports from the Democratic Republic of the Congo, the operators in the mining sector are hereby informed that on June 21, 2025, the Board of Directors of the Agency for the Regulation and Control of Mineral Markets (ARECOMS) adopted significant regulatory measures, the main points of which are outlined below:

1. In light of the persistently high inventory levels in the market, it has been decided to extend the temporary ban for an additional three months from the effective date of this decision. This extension applies to all cobalt exports originating from mining in the Democratic Republic of the Congo, regardless of whether they come from industrial, semi-industrial, small-scale, or artisanal mining operations.

2. The Mineral Products Control Agency expects to announce a new decision before the end of the suspension period. If necessary, this decision will modify, extend, or terminate this temporary suspension measure.

This decision shall come into force upon signature.

Policy Background:

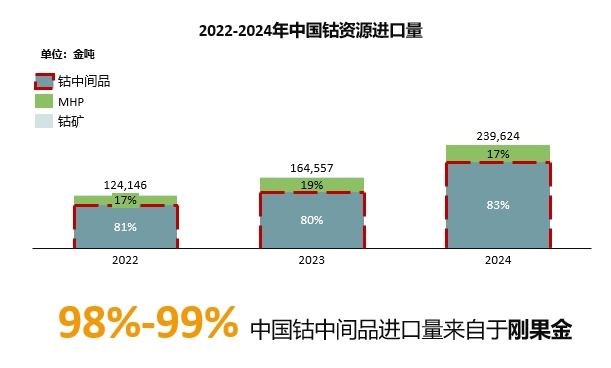

As the world's leading cobalt producer, the DRC is rich in cobalt resources. China, as one of the world's largest cobalt consumers, has long been highly dependent on cobalt raw material supplies from the DRC.

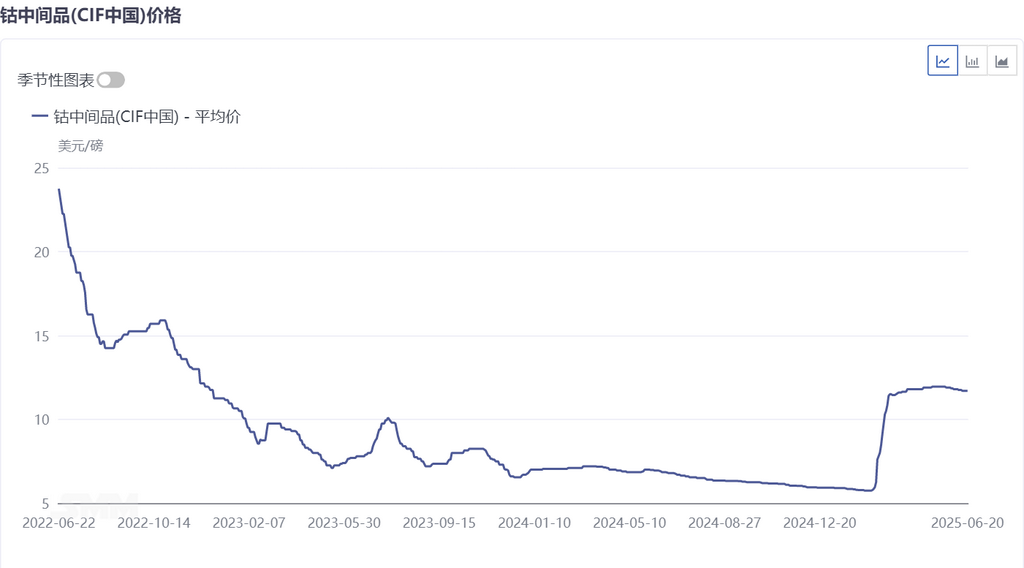

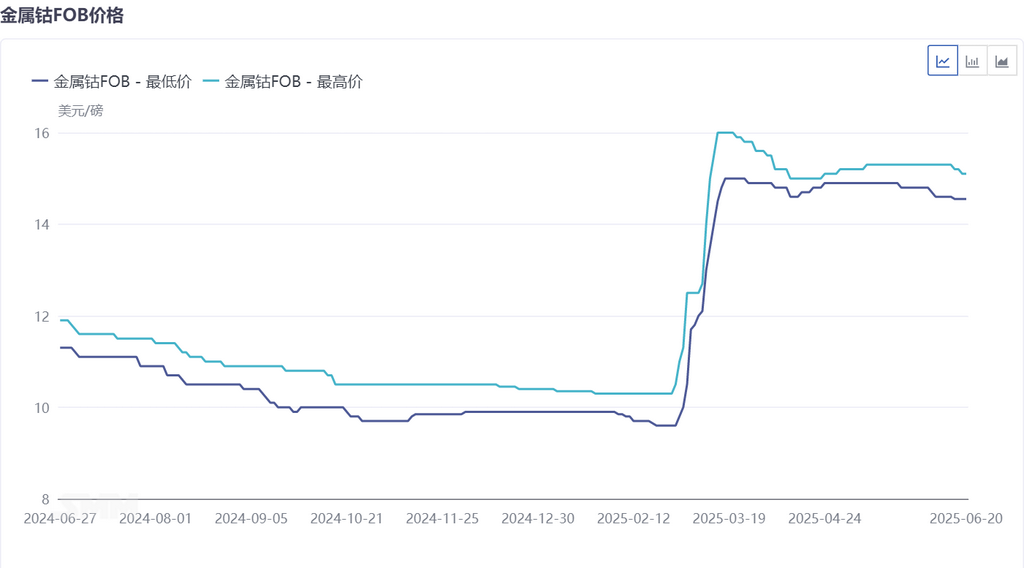

However, in recent years, the global cobalt market has continued to face supply surplus pressure, leading to a significant decline in prices. The international price of refined cobalt once dropped to a low of $9.6/lb, and the price of cobalt raw materials even fell to a low of $5.78/lb. The sharp decline in prices severely impacted the fiscal revenue of the DRC and the profitability of global cobalt smelters.

To address this dilemma, the government of the DRC implemented a cobalt export ban for the first time on February 22, 2025, aiming to:

-

Digest Excess Inventory: Reduce market supply and alleviate inventory pressure.

-

Boost Cobalt Prices: Stimulate price rebound by restricting supply.

The policy had significant initial effects: the international price of refined cobalt rebounded from $10/lb to $15/lb, and the price of cobalt raw materials also surged from $6/lb to $12/lb.

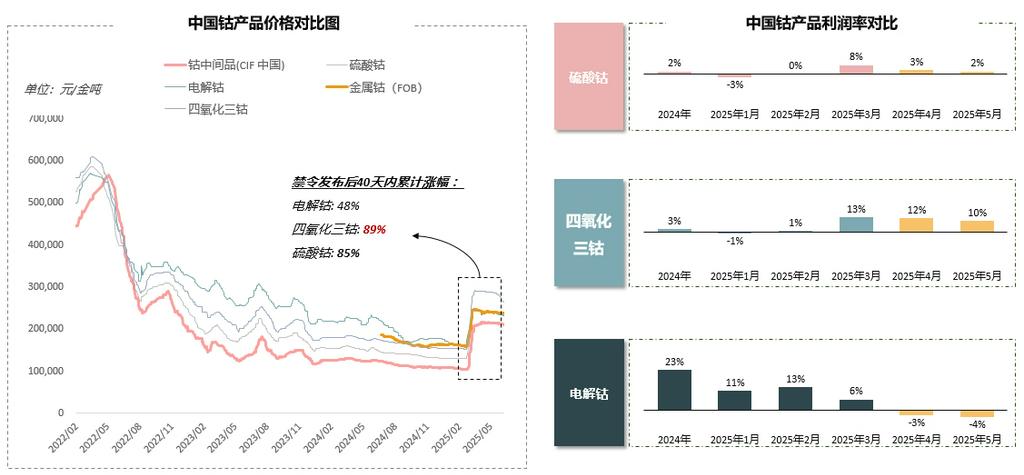

Under the influence of the ban, the domestic cobalt market in China also rose sharply, with the largest increases seen in Co3O4 and cobalt salt, which had relatively low inventory levels at that time.

However, the fundamental situation of supply surplus in the cobalt market has not yet been fundamentally improved. In light of this, the DRC government has decided to extend the export ban for three months. This move indicates that

- the global cobalt market's supply surplus situation has not been completely reversed.

- The DRC government hopes to further restrict supply to digest inventories and push up prices.

Impact of the ban extension:

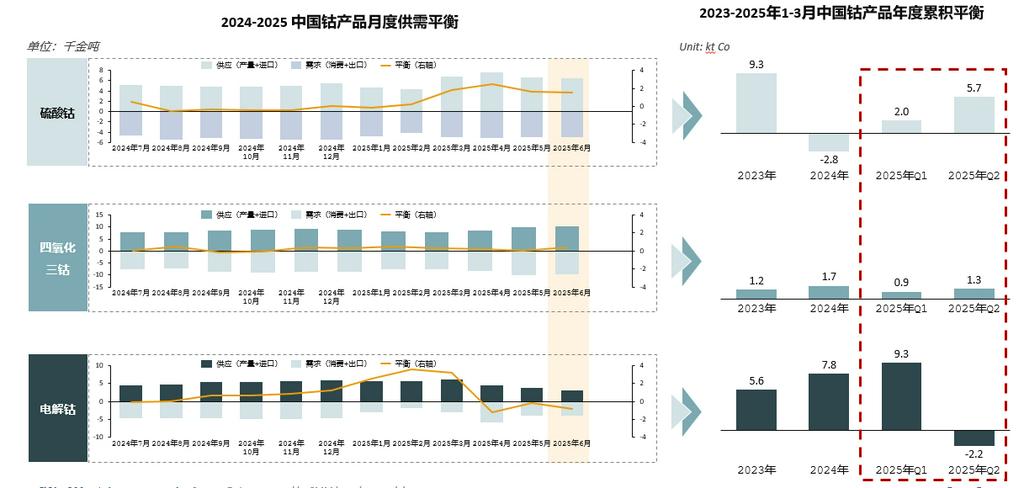

According to the SMM survey, current cobalt industry inventories are mainly concentrated in the upstream ore segments and downstream end-use products such as refined cobalt and batteries. Inventories in the midstream, including cobalt salt, cobalt tetroxide, and battery cells, are relatively low. Considering the inventories held by smelters and traders, we believe that Chinese smelter inventories will decline to a lower level in August-September. To avoid the risk of lower market inventories and further increases in procurement costs in the future, we believe that midstream cobalt salt, cobalt tetroxide, and ternary enterprises may increase procurement starting next week, and actual market transactions will improve.

- For Chinese smelters: In the short term, they can still maintain production relying on existing inventories. However, the extension of the ban exacerbates the uncertainty of raw material supply. In the coming months, enterprises may face the risk of raw material shortages and be forced to seek alternative sources or accelerate inventory depletion. Meanwhile, rising procurement costs will squeeze profits and may even lead to losses for some enterprises when producing refined cobalt in the later stages.

- For the DRC: Although the ban helps stabilize prices, it also means that the country will lose significant foreign exchange earnings from cobalt exports in the short term, increasing fiscal pressure and necessitating the search for other ways to fill the gap (such as increasing the mining of other minerals or adjusting taxes).

- For the global market:

- Supply tightness intensifies: The suspension of exports by the DRC will significantly tighten the global supply of cobalt raw materials.

- Short-term price support: Supply tightness is expected to support cobalt prices in the short term.

- Demand is key: Whether prices can continue to rebound ultimately depends on the growth momentum of global demand (especially in the EV sector). If demand is weak, price increases will be limited.

- Supply chain restructuring: It may stimulate other cobalt-producing countries (such as Indonesia) to increase production and prompt consuming countries to seek diversified supply channels.

- Downstream transmission: Fluctuations in cobalt prices will affect the cost structures of battery manufacturers and high-tech enterprises and may be transmitted to the prices of end-use products (such as EVs and electronic products). However, it should be noted that in recent years, due to the high cost-effectiveness of LFP batteries, the share of ternary batteries (NCM) in new energy vehicles (EVs) has been gradually squeezed year by year. This round of the ban pushing up cobalt prices may increase NCM battery prices, further suppressing their demand in EVs and accelerating the substitution of LFP for NCM.

Future Outlook:

Before the implementation of this ban, the market generally expected that the DRC's policy would be extended by two months. A three-month extension, to some extent, slightly exceeded market expectations. As the ban is extended and the inventory of Chinese smelters continues to deplete (expected to reach a low level by mid-to-late August), there is further upward momentum in the price of cobalt raw materials, driving up the prices of all cobalt products. However, this process will be gradual and highly dependent on the actual recovery of downstream demand. Excessively rapid price increases may suppress downstream demand, and if demand remains weak, price increases will be limited. Therefore, in the future market, it is still necessary to closely monitor the relationship between high cobalt prices and demand.

In summary, the DRC's extension of the cobalt export ban is a strong measure to address market imbalances and boost prices. Although it helps alleviate the supply surplus and support cobalt prices in the short term, it also puts pressure on the global supply chain (especially Chinese smelters) and may sacrifice the DRC's own interests. In the short term, it will not receive export revenue, and in the long term, if cobalt prices remain high, it may suppress cobalt market demand and reduce the DRC's export revenue. In the coming months, the global cobalt market will continue to seek a new equilibrium amid supply tightness and price fluctuations.

SMM New Energy Research Team

Cong Wang 021-51666838

Rui Ma 021-51595780

Disheng Feng 021-51666714

Yanlin Lv 021-20707875

Yujun Liu 021-20707895

Zhicheng Zhou 021-51666711

Wenhao Xiao 021-51666872